Back to Kaleidoscope Creativity overview

Kaleidoscope Creativity Attitudes

In this section

Characterised by their low cultural engagement, despite some considering themselves 'arty', they are easily put off by price, so are more likely to attend free events.

Priorities

Mainstream cultural provision is not a priority for this group, who tend not to identify with traditional offerings, but see themselves as arty in other ways.

- Despite many being creative, and some seeing themselves as 'arty', there’s often a rejection of traditional provision as ‘not for the likes of them’.

- This is likely to be an equal or stronger contributory factor than low income to their being amongst those least disposed to attend formal arts and cultural events in traditional venues.

- This incongruity suggests that there are artistic needs and aspirations that are not being met through present styles and levels of cultural provision and opportunity. See Sectors > Participation and Places >Provision & Community for more detail.

Spending

Most of the creative activities they engage with are free and a high price point for tickets will turn a probably not into a hard no.

- Expensively priced tickets will present a barrier for some in this group on low incomes, so a range of suitable price discounting options are likely to be necessary.

- In fact, some of the activities with which Kaleidoscope Creativity are most well-disposed to engage with tend to be free.

- Finding partners to enable free access, or other revenue streams (such as retail, donations, funding, or sponsorship) and volunteering opportunities to help facilitate this may be important.

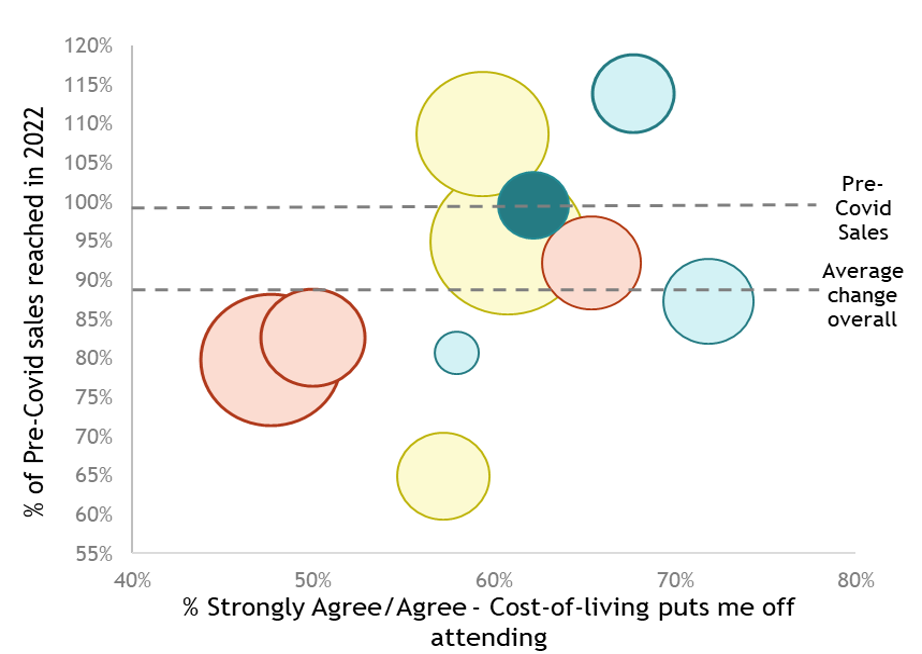

Cost-of-living concerns

Although Kaleidoscope Creativity's engagement has returned to pre-Covid-19 levels, their cultural participation has always been low and they are historically the most likely segment to be put off by price, as is reflected in their cost of-living concerns.

This group are similar to lower engaged groups in agreeing that changing interest and inflation rates will impact cultural spending but are less worried than most other segments about energy costs.